Home insurance is built to help homeowners recover from certain sudden and unexpected losses, but it is not designed to cover every problem a house may experience. For homeowners in Hickory, NC, understanding which events your policy is designed to protect against can make it easier to review coverage, prepare for claims, and avoid expensive assumptions.

What Home Insurance Coverage Events Mean

A coverage event is a cause of loss that may trigger protection under your home insurance policy. These are often called covered perils. Depending on the type of policy you have, coverage may apply to damage caused by fire, wind, hail, theft, vandalism, lightning, certain water damage, falling objects, or other listed or non-excluded events.

The direct answer is this: home insurance is generally designed to protect against sudden and accidental damage from covered events, not routine maintenance, wear and tear, neglect, or every type of natural disaster. The exact events covered depend on your policy form, endorsements, exclusions, deductibles, and coverage limits.

In our work with clients, a common issue we see is that homeowners know they “have insurance” but do not know what kind of events the policy actually covers. That can lead to confusion when damage occurs and the cause of loss becomes the main focus of the claim.

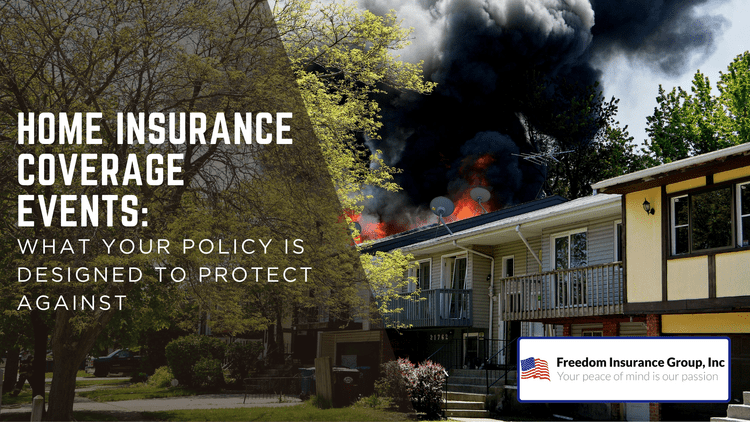

Fire And Smoke Damage

Fire is one of the core events most home insurance policies are designed to cover. A covered fire may damage the home’s structure, personal belongings, detached structures, and create additional living expenses if the home becomes temporarily unlivable.

Smoke damage can also be significant. Even if flames are contained to one area, smoke can affect walls, ceilings, furniture, clothing, electronics, and HVAC systems.

After a fire or smoke event, homeowners should document damage carefully, avoid throwing items away too quickly, and follow the insurance company’s claim process. Professional cleaning, restoration, and inspection may be needed before the home is safe to occupy again.

Wind And Hail Damage

Wind and hail are common causes of home insurance claims. Strong wind can damage shingles, siding, gutters, fences, windows, and detached structures. Hail can dent roofing materials, damage skylights, crack siding, and harm exterior property.

For homes near Viewmont or around Union Square, storms can move through quickly and leave behind damage that is not always obvious from the ground. After a major storm, it may be worth checking for missing shingles, damaged gutters, broken branches, and water stains inside the home.

Policy details matter. Some policies have separate wind or hail deductibles. Others may treat roof damage differently based on roof age, material, or condition. Homeowners should review whether roof claims are handled on a replacement cost or actual cash value basis.

Lightning Damage

Lightning can damage more than the exterior of a home. It may affect wiring, electrical panels, appliances, computers, televisions, garage door openers, HVAC systems, security equipment, and smart home devices.

A direct strike may leave visible evidence, but surge damage can be harder to prove. If several electronics or appliances fail after a storm, document the timing, take photos, and obtain technician reports when possible.

A home insurance policy may cover lightning-related damage, subject to the deductible and policy terms. Equipment breakdown or service line endorsements may also be worth reviewing, depending on the home’s systems and the type of damage.

Theft And Vandalism

Home insurance may help cover stolen personal property and damage caused by theft or vandalism. This can include broken doors, damaged locks, smashed windows, stolen electronics, missing tools, or damaged personal belongings.

After a theft or vandalism event, homeowners should file a police report, take photos, make a list of stolen or damaged items, and gather receipts or proof of ownership. Security camera footage, online order histories, warranty records, and photos of belongings can help support the claim.

Valuable items may have special limits. Jewelry, firearms, collectibles, art, cash, and certain electronics may not be fully covered unless scheduled or endorsed. Homeowners in Hickory, NC should review these limits before a theft happens, especially if they own high-value items.

Certain Types Of Water Damage

Water damage is one of the most misunderstood areas of home insurance. Many policies may cover sudden and accidental water damage, such as a burst pipe, failed appliance hose, or accidental discharge from a plumbing system.

However, gradual leaks, seepage, flooding, poor maintenance, sewer backup, and water entering from outside may be limited or excluded unless specific coverage is added.

Examples of water losses that may be treated differently include:

- A pipe suddenly bursts behind a wall

- A washing machine hose fails unexpectedly

- A slow leak under a sink causes long-term cabinet damage

- Heavy rain causes water to enter through the foundation

- A sewer or drain backs up into the home

- Floodwater enters from outside

The source and timing of the water matter. A sudden pipe break is different from a leak that has been present for months. Homeowners should act quickly to stop water, document damage, and begin reasonable mitigation.

Falling Objects And Tree Damage

Home insurance may cover damage from falling objects, such as tree limbs, branches, or debris, if the cause of loss is covered. If a tree falls on the home during a storm, the policy may help pay for repairs to the damaged structure, subject to policy terms.

Tree removal coverage can be limited. If a tree falls in the yard without damaging covered property, the policy may provide little or no payment for removal. If it damages the roof, fence, garage, or other covered structure, coverage may be different.

Maintenance can also matter. If a tree was clearly dead or hazardous and ignored for a long period, the claim may receive more scrutiny. Homeowners should keep trees trimmed and address visible hazards before storms arrive.

Liability Events

Home insurance is not only about property damage. It also includes personal liability coverage, which may help protect you if someone claims you are legally responsible for injury or property damage.

- Liability events may include:

- A guest trips on a broken step

- A visitor is injured on the property

- A dog bite claim

- Accidental damage to someone else’s property

- Certain incidents away from the home

Liability limits should be reviewed carefully. Serious injuries can exceed basic limits, and a personal umbrella policy may be worth considering for added protection.

Additional Living Expenses

If a covered event makes your home temporarily unlivable, additional living expenses coverage may help pay for extra costs while repairs are completed. This may include hotel stays, temporary rentals, increased meal costs, laundry, storage, or other necessary expenses above your normal living costs.

This coverage is usually tied to a covered property claim. If the damage itself is not covered, additional living expenses may not apply.

Events Home Insurance Often Does Not Cover

Home insurance has exclusions. Common exclusions may include:

- Flooding from outside water

- Earthquake damage

- Wear and tear

- Mold from long-term moisture

- Pest damage

- Neglect

- Intentional damage

- Sewer backup without endorsement

- Business property beyond policy limits

- Certain vacant-home losses

These gaps can often be addressed with separate policies or endorsements, but they should be reviewed before a claim.

Conclusion

Home insurance is designed to protect against covered events such as fire, smoke, wind, hail, lightning, theft, vandalism, certain water damage, falling objects, and liability claims. It is not designed to cover every maintenance issue, gradual problem, or excluded disaster. For homeowners in Hickory, NC, reviewing coverage events, exclusions, deductibles, and special limits can help you understand what your policy is built to do before damage occurs.

At Freedom Insurance Group, Inc., we aim to provide comprehensive insurance policies that make your life easier. We want to help you get insurance that fits your needs. You can get additional information about our products and services by calling our agency at 828-322-7474. Get a free quote today by CLICKING HERE.

Disclaimer: The information presented in this blog is intended for informational purposes only and should not be considered as professional advice. It is crucial to consult with a qualified insurance agent or professional for personalized advice tailored to your specific circumstances. They can provide expert guidance and help you make informed decisions regarding your insurance needs.

Freedom Insurance Group, Inc.

Hickory, NC

828-322-7474